ROSE Insights

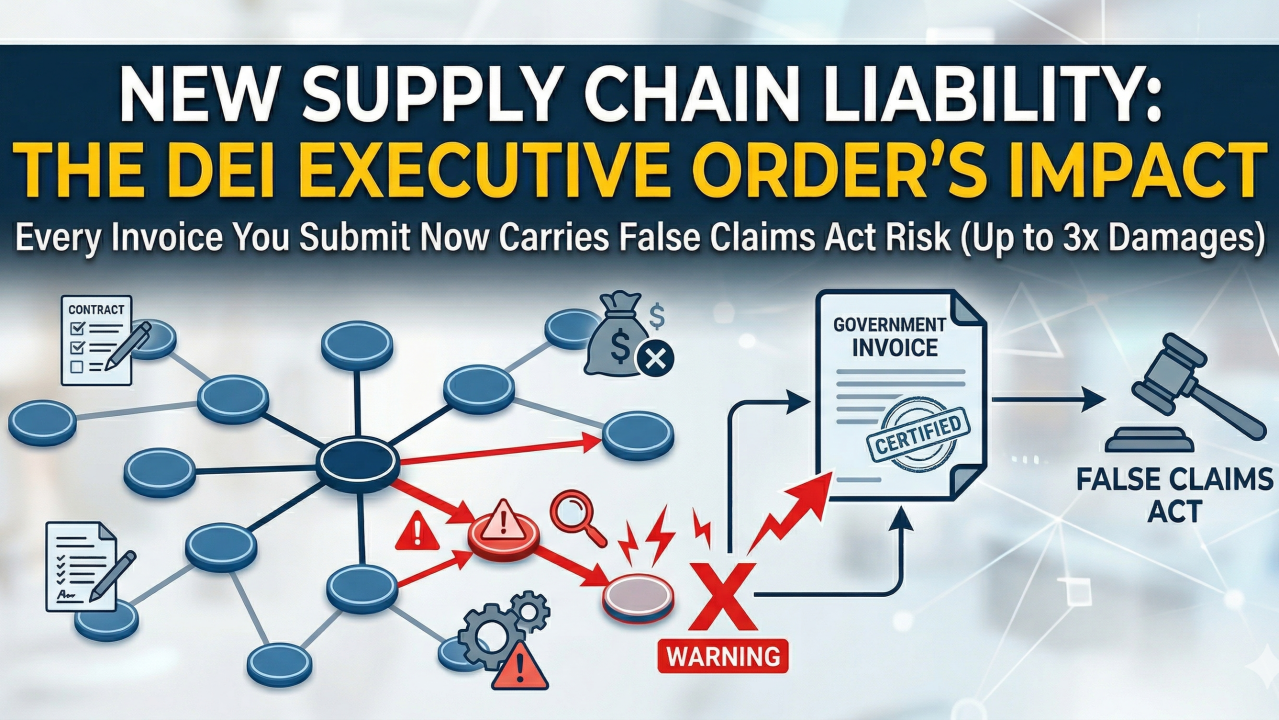

New federal contract clauses make supply chain compliance material under the False Claims Act, exposing primes to treble damages, penalties, and audit risk.

Most growing organizations don't discover gaps in their financial systems until something forces the issue; an audit, a capital raise, a key person leaving, or a contract they're not equipped to manage. The Financial System Readiness Review exists to surface those gaps before they become expensive. In this video, Ted Rose walks through what the FSRR actually evaluates, why looking at your accounting software alone isn't enough, and how the three-step process produces a roadmap that tells you exactly what to fix, in what order, and why it matters for where your organization is headed.

Learn what a strong finance structural foundation includes: governance, segregation of duties, internal controls, and compliance readiness for audits.

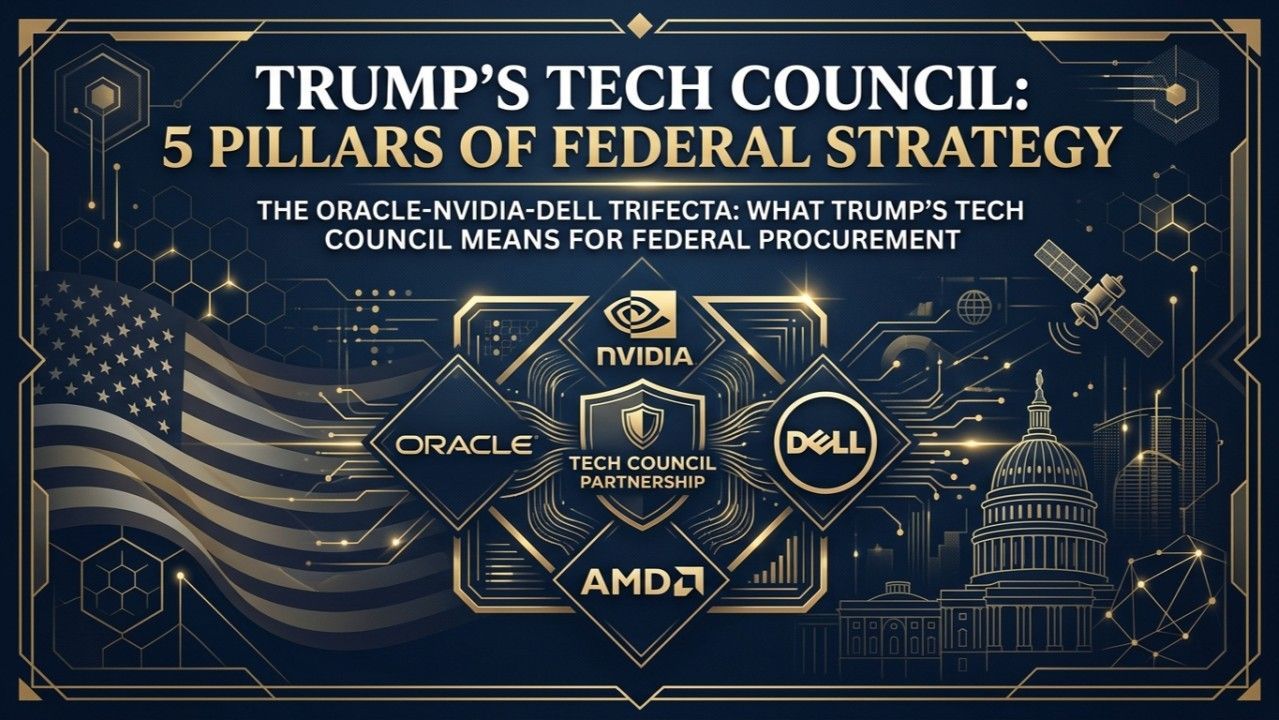

A new U.S. tech advisory council stacked with Oracle, NVIDIA, Dell and AMD signals shifts in federal procurement toward AI, quantum, fusion energy and crypto.

Most CEOs don’t fully trust their financial data, leading to slower decisions and missed opportunities. Learn how to close the trust gap and build decision-ready finance.

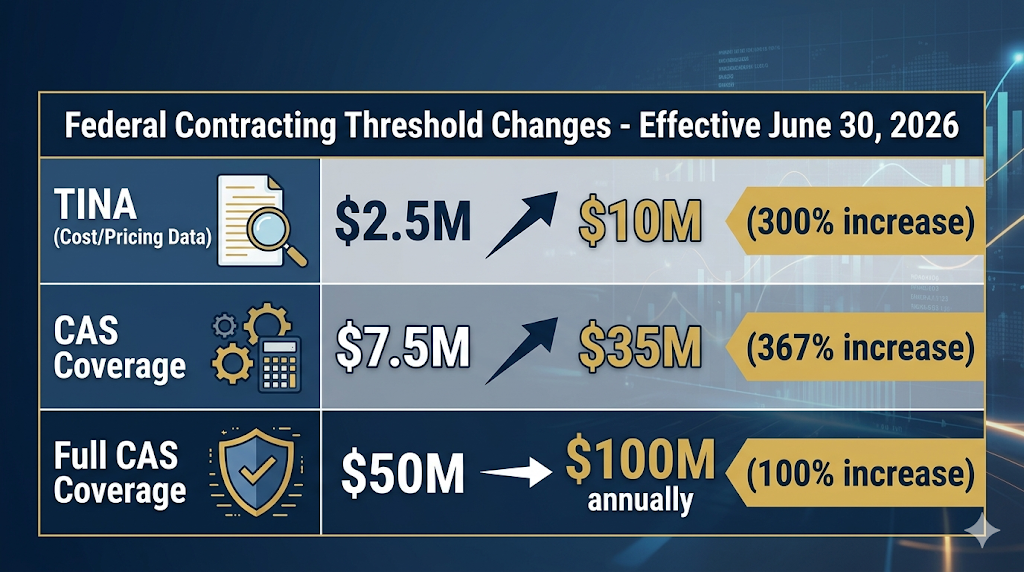

A deep dive into how DOGE cuts, 8(a) program changes, and new federal thresholds are reshaping small business government contracting in 2026

By WALLY ANGEL , ROSE FINANCIAL SOLUTIONS

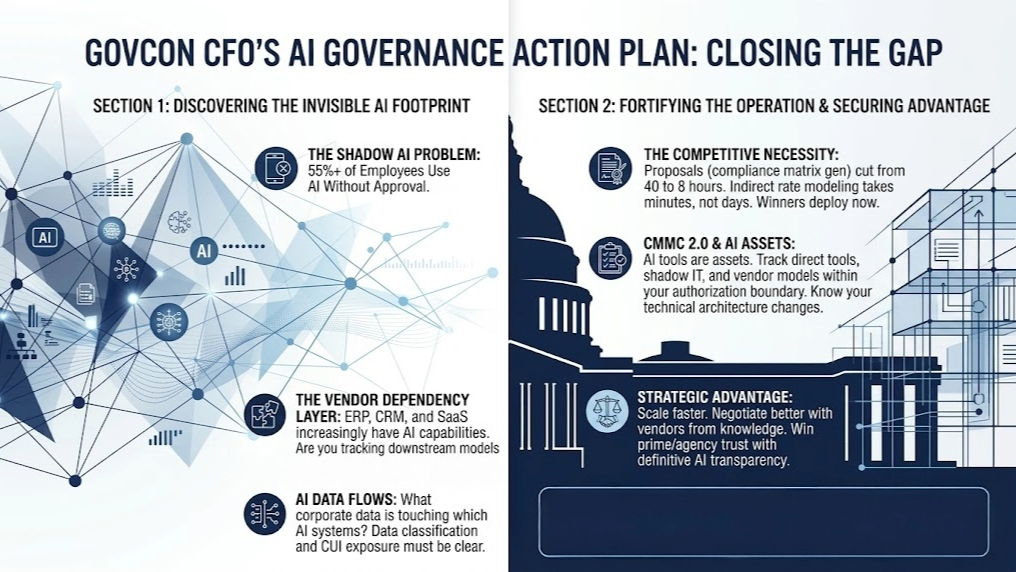

AI in finance starts with strong systems. Learn why most companies are not ready and how to build a decision-ready financial infrastructure.

By TED ROSE , ROSE FINANCIAL SOLUTIONS

Get More Financial Insights

Ready to gain financial clarity and take control of your financial future? Reach out to us now by filling out this contact form. Our team is here to answer your questions and guide you toward a brighter financial horizon.

Let's start the conversation today!