Government Contract (GovCon) Accounting Services

Trusted by clients like you for nearly 30 years.

Focus on Winning Government Contracts

Let Us Handle Your Financial Complexities

Many government contractors believe they must use a specific accounting software package to be deemed DCAA compliant. All of ROSE’s client systems have been approved by the DCAA when audited—100 percent of the time, regardless of the accounting database used. Our leading-edge platform, Easby, supports most accounting software systems. With our FaaS solution, your DCAA compliance will be enhanced, and you’ll also gain the functionality found in an Enterprise Resource Planning (ERP) system.

Maintaining government contract compliance is complex and requires financial discipline.

Our GovCon clients have a 100% DCAA/Audit pass rate.

Go after any contract type with confidence.

Set up, maintain, and scale a DCAA/GovCon compliant accounting system.

Improve cash flow and profitability with expert GovCon pricing and indirect rate support.

Our services adhere to strict CMMC standards, ensuring your financial data meets contracting requirements.

We scale with you, providing continuous support as your company grows from startup to $200+ million.

Finance as a Service (FaaS) for Government Contractors

Getting started with ROSE®

Experience the difference that our GovCon expert and leading-technology can make.

Schedule a Call

A quick introductory call can give you the information you need to determine what's possible with FaaS.

Assess Your Needs

Assess your options and determine whether you require a comprehensive solution or simply need to fill in the gaps where your existing team and systems need support.

Implement Your Solution

Implement your solution with a seasoned team of experts who not only execute your solution but also provide ongoing support month in and month out.

Our Government Contract Accounting Software Partners

For Start-Up to Mid-Sized GovCon's

Full or partial ROSE FaaS Solution Plus:

- Conversion to or optimization of Quickbooks

- Integration of Easby to support meaningful financial reporting that is timely and accurate

- Cost-effective and scalable Quickbooks solutions

- Minimize GovCon/DCAA compliance-related risks

For Small to Mid-size GovCons

Full or partial ROSE FaaS Solution Plus:

- Conversion to or optimization of Procas

- Integration of Easby to support meaningful financial reporting that is timely and accurate

- Cost-effective and scalable Procas solutions

- Minimize GovCon/DCAA compliance-related risks

For Small to Mid-size GovCons

Full or partial ROSE FaaS Solution Plus:

- Conversion to or optimization of Unanet

- Integration of Easby to support meaningful financial reporting that is timely and accurate

- Cost-effective and scalable Unanet solutions

- Minimize GovCon/DCAA compliance-related risks

For GovCons Preparing for Scale

Full or partial ROSE FaaS Solution Plus:

- Conversion to or optimization of Deltek Costpoint

- Integration of Easby to support meaningful financial reporting that is timely and accurate

- Cost-effective and scalable Costpoint solutions

- Minimize GovCon/DCAA compliance-related risks

Top GovCon Questions, Answered

The right knowledge now saves time and money later. Check out our GovCon FAQs for practical, CFO-level guidance that helps you build a strong financial foundation.

Outsourced Accounting Can Be Tailored into Comprehensive or Functional Solutions for GovCons

Project Reporting

Project Forecasting and Burn Rate

Indirect Rate Reporting

Labor Distribution

Billing

Cash Receipts and Deposits

Accounts Payable

Bill Payment

Credit Card Expense Management

Payroll Administration and Processing

Time System Administration

Expense System Administration

Monthly Closing

Financial Reporting

Management Reporting

Financial Analysis

GovCon Solutions for Your Business

GovCon Support

- Contract Administration Assistance

- Questions on DCAA Compliance

- Contract Review

Annual Budget

- Preparation of Annual Operating Budget

Provisional Rates

- Indirect Rate Pool Development and Analysis

- Provisional Rate Submissions

Proposal Support

- Cost Proposal Preparation & Review

- CAS and FARS Support Related to Your Specific RFP

- Negotiations with Contracting Officers

Incurred Cost Submission

- Assistance in Year-End Review of Contracts and Records

- Prepare Incurred Cost Electronic (ICE) Schedules

- Interface Directly with DCAA Regarding Submission

Contract Reconciliations

- Preparation of Adjustment Vouchers

- Analysis of Rate Variances

- Assistance with Contract Close Out

Accounting Manual

- Policies and Procedures Manual Development

- Annual Policies and Procedures Manual Update

DCAA Audits and Reviews

- DCAA Audit Interface/Assistance

- Pre-award

- ICE Audits

Letter of Adequacy

- Review Accounting Policies and Procedures in Accordance with the DCAA Audit Program

The Benefits of Outsourced CFO Services for GovCons

Government contractors (GovCons) often encounter unique financial challenges that demand expert-level GovCon CFO support. Outsourced fractional CFO services offers GovCons a powerful solution to navigate regulatory complexities, improve compliance, manage growth and risk, and improve financial capability. Leveraging outsourced financial management can ensure your business stays on track while driving long-term success.

Pricing Support for Government Contracting

Developing compliant and competitive pricing for government contracts is essential for success in the GovCon space. Proper pricing support involves understanding the complexities of FAR requirements, indirect rate structures, and cost allocation. With the right pricing strategy, GovCons can improve their contract-winning potential while maintaining profitability and compliance with government standards.

Audit Readiness Services for GovCons

Government contractors (GovCons) must be fully prepared for the rigorous audits required by federal regulations. Effective audit readiness means maintaining organized financial records, ensuring strict adherence to DCAA standards, and implementing proper internal controls. By focusing on proactive audit preparation, GovCons can minimize risks, avoid costly penalties, and streamline the audit process when it arises.

Easby Makes it Easy

Our FaaS solution, Easby, combines people, process, technology, organization, and data. to simplify and automate accounting functions, ensure compliance, and deliver strategic guidance and financial analysis from a team of top finance and accounting professionals.

Our Finance as a Service (FaaS) Solutions

Whether you are seeking full-service government finance and accounting solutions or want to choose the solution that best fits your company’s needs, turn to ROSE for the financial clarity you need to make confident business decisions and achieve more—all at the fraction of the cost of managing these processes internally.

Outsourced CFO and Financial Management Solutions

Our fractional CFO and financial management services provide you with financial clarity to make confident business decisions.

Accounting & Functional Services

We’re leading the paradigm shift from traditional outsourced finance & accounting services to Finance as a Service (FaaS).

Tax & Compliance Services

We tailor our tax and compliance solutions to each client’s needs based on their current needs as well as their future plans. Regulation compliance include federal taxes, state and local jurisdictions, Federal Acquisition Regulations, DCAA, and more.

The ROSE® Difference

Industry Pioneers.

For over thirty years, ROSE has been building financial systems and best practices specifically designed for government contractors (GovCons). We are at the forefront of Finance as a Service (FaaS), providing the People, Process, Technology, Organization, and Data to enhance financial efficiency, compliance, and scalability for GovCons looking to drive sustainable growth.

Trusted Advisors.

At ROSE, our experienced team of GovCon finance, accounting, and tax professionals delivers mission-critical financial guidance to government contractors. As trusted advisors, we the guidance and financial discipline that GovCons need to meet compliance requirements, financial growth, and profitability goals.

Cost Effective & Scalable.

ROSE provides a scalable, cloud-based financial infrastructure designed for cost efficiency. Our solutions save GovCons 20 to 50 percent compared to in-house management, allowing your business to focus on core competencies.

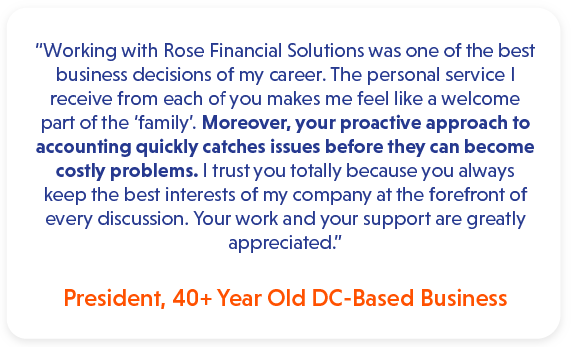

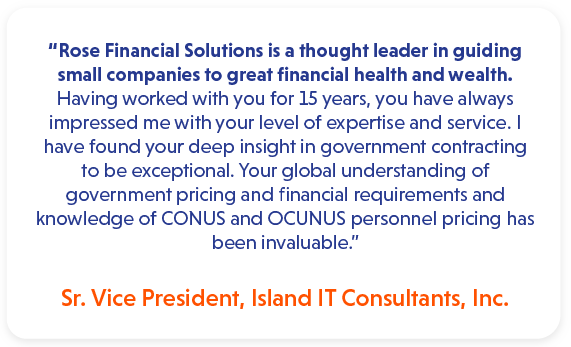

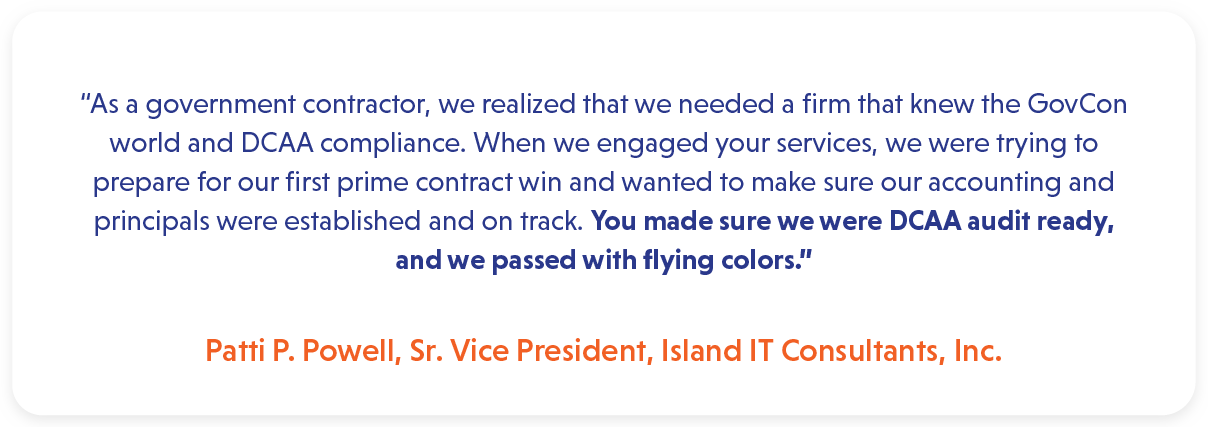

In Our Client's Words

Read what our satisfied clients have to say about their experiences with us. Your success story could be next!

ROSE Insights

Start your path to financial success and security now – take the first step by diving into our extensive collection of articles, tips, and expert advice. Don't miss out on the opportunity to bring clarity to your financial future!

How can we help you achieve financial clarity?

Ready to gain financial clarity and take control of your financial future? Reach out to us now by filling out this contact form. Our team is here to answer your questions and guide you toward a brighter financial horizon.

Let's start the conversation today!